January 2015 Side Hustle Income Report

This will be a tough post to write. Not because the news contained within is shocking or surprising, but because it is the first time I've been completely, totally, 100% honest my own money choices. Here is my deepest, darkest, dirtiest secret about my finances….

My Darkest Financial Secret

For those just tuning in a little back story: I bought my first home in July 2013. I funded the renovation with a 203k loan, but went over and had to raid my savings account to finish the project. Having no savings cushion then led me to lean on my credit cards for “emergencies” in the Fall of 2013 and by NYE 2014, I was 8,432.16 in debt.

I was doing well on repayments, until the summer. My beloved dog died, my identity got stolen, and I had an intense falling out with a roommate all within the span of three weeks. On top of everything else I was still dealing with from Fall 2013 (broken engagement, runaway renovation), it felt like a ton of bricks.

And if you've been reading here for a while, you know that I have a problem with shopping my feelings. Which is exactly what I did.

At the end of July I was $10, 832.14 in debt, almost 3k up from where I was in April.

For shame!

One year later, by Fall 2014 I was feeling better and I managed to make some progress on my debt repayment.

- I paid back my parents in full.

- I paid off my small, lingering, student loan. (The smartest decision I made was paying off accounts that couldn't be racked up again, so that debt is now gone for good!)

- I saved enough money to put down a sizable down payment on a new-to-me car I bought in November that I desperately needed.

Between my savings, my home appreciation, and my winning retirement accounts, my net worth did increase over the year.

All-in-all there were some financial victories in 2014.

But ultimately, 2014 was a year of financial failure.

Honestly, I was too enthralled with the emotional things that were going on around me to pay too much attention to where my money was going. I am disappointed that for years I've prided myself on being a go-getter and a goal reacher, and my biggest financial goal in 2014 was to pay down all of my debt. I did not get there. Not even close.

I ended 2014 $8,164.97 in debt (does not include car loan.) This is only $300 less than where it was when I started.

Because I use my YTD spending tracker, I was, however, able to see how much I did put toward my cards. I made $11,011.54 in credit card payments this year, which would have been enough to cover all of the debt and then some.

How? Why?

Put simply: I was paying off debt, but only at the rate at which I was spending.

Please let this be a lesson to those of you working your way out of debt right now: STOP USING YOUR CARDS. You will never get anywhere if you don't.

Currently, mine are in my freezer. As a New Year present to myself, I put $1,000 from my savings to my debt on January 2nd.

So as of right now, my debt sits at $7,164.97.

And as of January 1, 2015, I'm on the Spending Diet, as created by the lovely Anna Newell-Jones. The gist of it is that you only spend on necessities, and give yourself $100 of “play money” each month. This is different than the spending fast where you don't spend anything except what it costs for rent/utilities/gas and groceries. That seemed a little too strict for me to begin with, but I liked the idea of the diet, so I'm trying it out.

- Halfway through the month, it is going OK.

- I've also set a pretty lofty goal of trying to pay down all of my debt by March 31.

- Math-wise means I have to put $1200 toward my debt every fifteen days (and then a little extra at the end.)

It's ambitious for sure, and I don't know what life is going to throw my way, but that is why I am sharing it with you all….to put it all out there and keep me accountable once and for all. I hope this inspires some others out there battling with recurring credit card debt to join my movement, throw the cards in the freezer, and get free once and for all. This is Part 1 of what I'm calling the LBMT- Get Debt Free Plan.

January 2015 Side Hustle Update

I have multiple income sources of income:

- A full-time job

- Rental income from my house

- Freelance writing

- Income generated from activities on this blog

- Selling no longer used items on Craigslist, Ebay, and TheRealReal

In January 2015 I made $3,216.51 in “extra” income outside my 9-5

Holy mambo Batman. This number is so, so incredible to me because it encapsulates an entire thirty days of focus and hard work. It's even more astounding that just a year ago that was more money than I made in a month at my full-time job. Just goes to show you that ANYONE can grow their income.

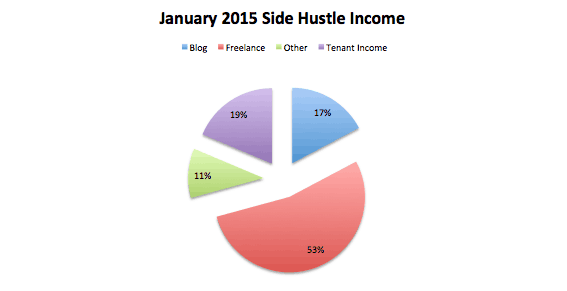

Here's how my numbers break down. Please keep in mind these numbers are BEFORE taxes and other business-related expenses.

- Freelance Income: 1721.51

- Blog Income (Advertising and Affiliate Income): 555.00

- Tenant Rent: 600.00

- “Other” Income: My brother bought my old car and I did a little freelance voice over work for a friend, ($340)

Here's a pie chart of my total side hustle income pie.

Debt Payoff Update

- After taxes and business expenses, I was able to put $2750 of my (~$3200) side income to my debt this month. I also contributed $400(ish) extra from my paychecks, and also pulled $300 from savings. Total paid toward debt in January? $3451.89

- Total percentage of debt paid off in January? 48%

Holy shit.

I swear that I'm not pretending to be amazed, I just actually can't believe I did it. I didn't even really think about the money I was earning, just that I knew I had a goal in mind. So, I kept my head down and kept moving. It wasn't until I sat down to tally up the numbers this AM and pay off the balance on my Chase card that I saw how far I'd come in just 30 short days.

A Few Final Notes

- I'm not gonna lie, it was a ton of work. But the feeling of getting things paid off is even better. Saying you're going to do something difficult and sticking to it also makes you feel a bit like a bad ass.

- I would have been able to contribute even more to my debt in January, but I had about $1345 dollars of home repairs (garage/junk clean up and rat infestation in the attic…. awesome) to take care of.

- Most of the repairs were cashflow-ed by the money I saved doing a No Spend Challenge.

- I was nowhere close to staying on track with my $100 of spending money each month. But I did manage to cut my discretionary spending by two-thirds, which is incredible progress for me. Cutting back did help me stay on track with my goals. Here's how I did it.

- Here's how I ramped up my side hustle.

I'm excited about what February has to bring. I've already got $1700 in projected revenue for the month and it's not even February 1st yet (as I write this for publication on Monday.) It's very exciting to see the focus and hard work you put into something being returned. There isn't anything better!

P.S. Here's my February and March debt repayment/side hustle income updates.

P.P.S. Did I complete the challenge? Find out here.

Lauren Bowling is the creator of Financial Best Life. Writing about money since 2012 (formerly as L Bee and the Money Tree), Bowling is an award-winning blogger and money and real estate expert whose advice has been featured on CNBC, Forbes, CNNMoney, Elite Daily, Business Insider, Redbook, and Woman’s Day Magazine and more. After selling the site to a division of The Motley Fool in 2019, Bowling is now back as the owner and primary voice behind FBL and is excited to continue educating elder millennials everywhere about how to afford their best life.