Want to Pay Off Debt Quickly? Here’s the 90-Day Plan That Actually Worked

2025 Update: Back when I first tackled that $8,000 debt in just 90 days, it felt like a monumental feat. Fast forward to 2025, and the tools and strat...

2025 Update: Back when I first tackled that $8,000 debt in just 90 days, it felt like a monumental feat. Fast forward to 2025, and the tools and strat...

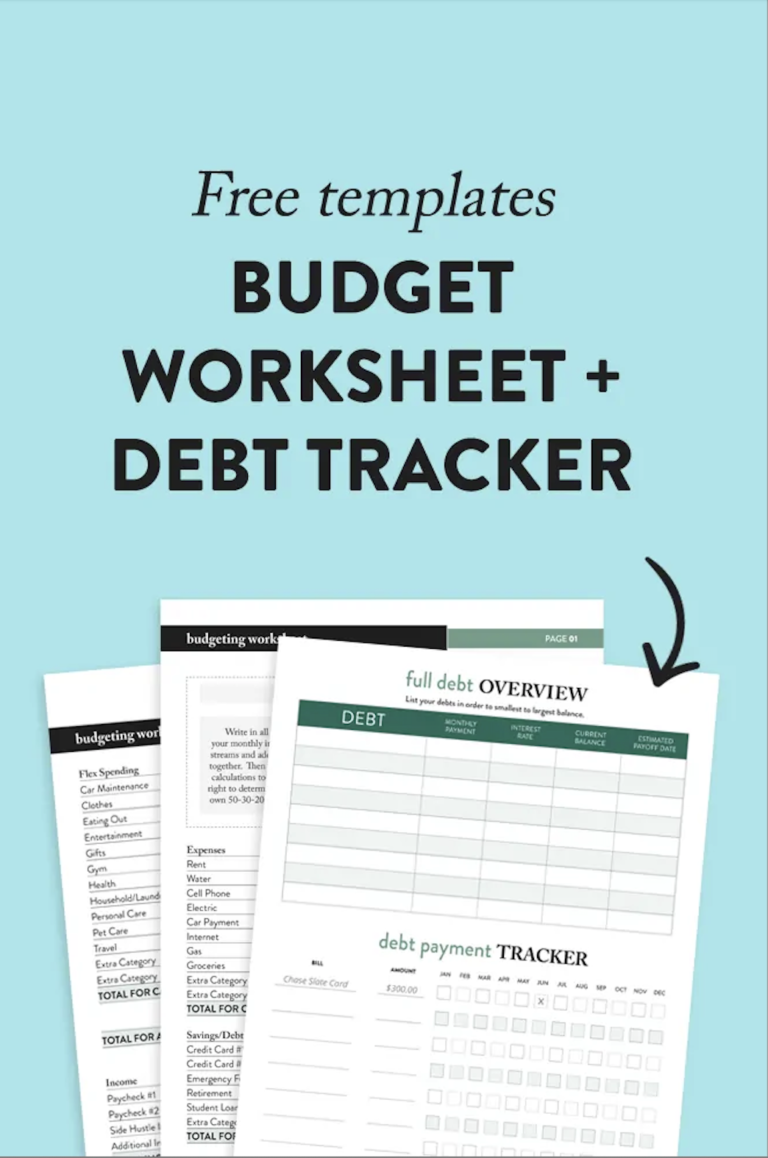

2025 Update:If you’re anything like me, you’ve tried a bunch of budgeting apps and spreadsheets that felt overwhelming or… just didn’t stick. ...

2025 Update: Private student loans are still the worst—no forgiveness, fewer protections, and a whole lot of fine print. But here’s the good news:...

Albert Einstein once said, "Compound interest is the eighth wonder of the world. Those who understand it, earn it…&nbs...

If you're just joining me for my side hustle income updates, here's a recap. At the beginning of the year, (2015) I was $8,164.97 in debt. After ...