After Years of Testing, These Are the Best Money Saving Apps I Still Use (2025)

2025 Update:

Five years, dozens of downloads, and one reformed overspender later… here’s what’s still on my phone. The personal finance app space has exploded, but honestly? Most of them are either clunky, confusing, or guilt-trippy. So I’ve narrowed it down to just the ones that actually helped me change my habits and save money without making me feel bad about iced coffee.

In 2025, I’m all about apps that give you clarity without the shame spiral. Whether you’re trying to automate savings, track spending, or just get your money organized, these tools have stood the test of time in my own budget. I’ve also added notes about what’s new or better this year — because if an app isn’t evolving, it’s not worth your time. Let’s cut through the noise and find what really works.

In full transparency, the only money-saving app I'm still using consistently month-to-month is Qapital. (You can also see the full list of other financial tools and products I use here.) I'm a big fan because it really helps me squirrel away money for my short-term goals: beach vacation, divorce party, new crop of clothes. It does all the heavy lifting for me (hence the word automatic) and it's made such a big difference in my ability to save consistently and spend wisely. Even though it does cost a few dollars each month, I can't recommend it enough.

The Best Money Saving Apps to Increase Your Bank Accounts

Acorns

How it saves money: After linking your primary spending account to the app and it will then round up transactions to the nearest dollar. Then they money gets invested.

Why I like it:

- Let's say you buy a coffee for $2.09 Acorns will take an additional $0.91 and put it into their individual investment account, just for you.

- This may not sound like much but if you bought that same cup of coffee 5 days a week for 1 year, then you will have invested $236.60 with just that one daily item. If we assume a compound interest rate of return of 8%, in one year, that $236.00 will become

- Price: $1 per month for all accounts under $5,000.

The TL:DR: Acorns has bank-level security and is a great way to learn about investing and put away spare change into investments if you want to learn about making your money grow. Click here to get started with Acorns.

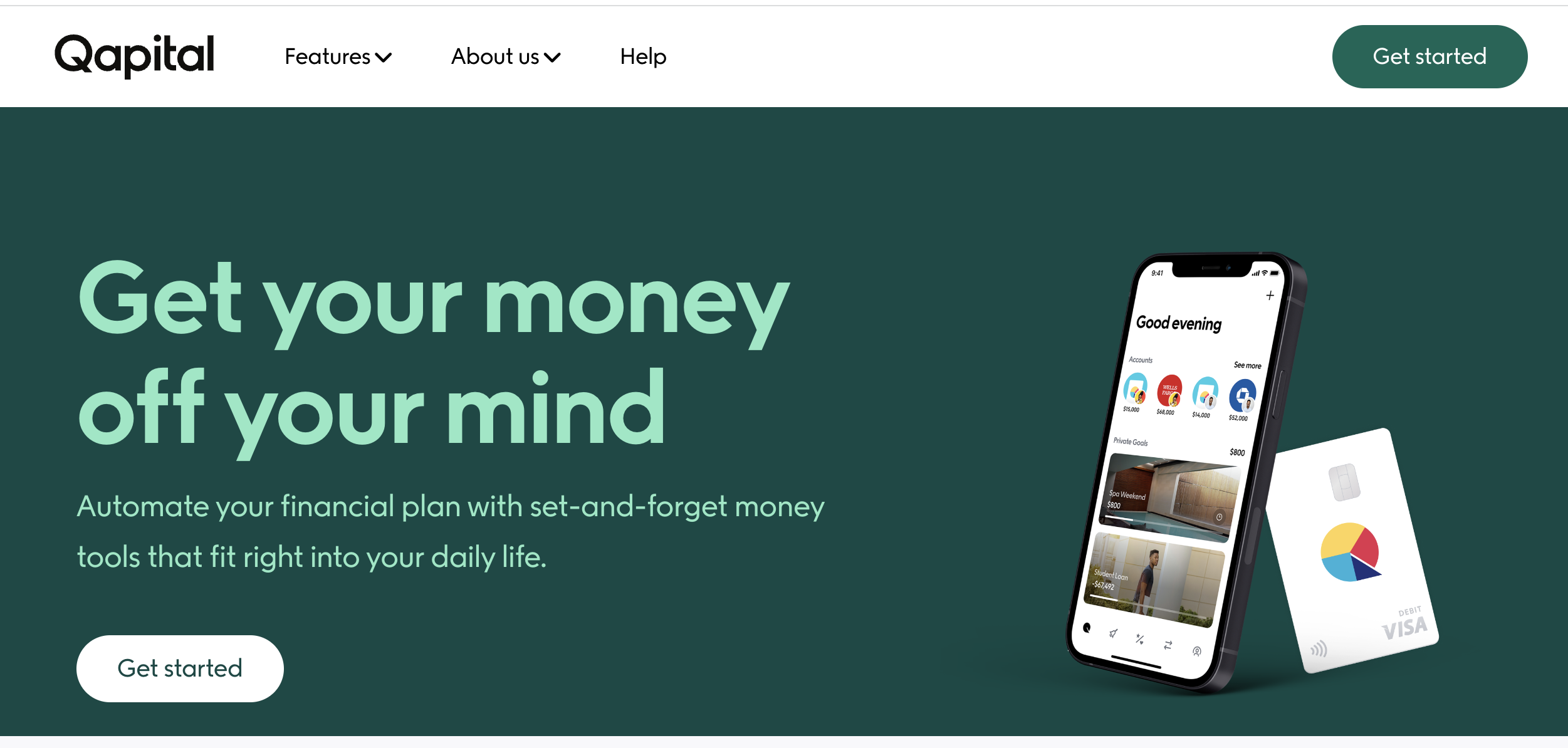

Qapital

How it Saves Money: If you need to gamify your goals in order to accomplish them this may be the best money-savings app. Qapital heavily relies on “If this then that” – (IFFT) technology, so you can save when you set certain behaviors. This is my FAVORITE money-saving app and the one I consistently use the most.

Why I like it:

- If you want to save money for a vacation, simply go into the Qapital app, set the amount, and then set the rules in which it will save money.

- It has a variety of “Savings rules” you can set to maximize how much you're putting away: you can make it so that if you meet a step goal through the pedometer on your phone that you save $1, $2, or even $10. Or it can automatically divide your paycheck.

- It can also save “roundups” on your purchases from your checking account. All of this is done automatically through the app and it is MAGIC.

- This is hands down my favorite “round up savings” app. It really helped me to keep saving even during the confusion that was sorting out my finances post-divorce. I love Qapital, and I tell everyone.

- I used Qapital to help me save 1000 in under a month and to save up $800 quickly for my divorce party. It works!!

- Price: Tiered membership $3-$12 per month.

The TL:DR Consider giving Qapital a try, (especially if you struggle with saving each month). It's one of my favorite money apps. It's free for the first month and then $3 thereafter. I saved $75 my first month with Qapital and the best part is that I didn't feel it. Click here to sign up for Qapital and get $25 for your goals by using this link.

Albert

How it Saves Money: It saves money by “sneaking” little pockets of money away from your checking account (Similar to Qapital et. al), but what's nice about this one is it can house your budget, saving contributions, and other financial accounts in one place.

Why I like it:

- This is a new-to-me app and I can't stop talking about it, playing with it, everything.

- I've never had a financial app that was this comprehensive.

- Over time it analyzes your spending and lets you know about important trends and if you're staying on track with your budget (which it also sets up for you based on current spending – automatically.)

Price: FREE! Although if you opt to do the text service, “Albert Genius”, you select an amount to pay that you feel is fair.

Other Favorite Money Saving Apps

Ibotta

How it Saves Money: Saves money in three ways: cashback on products at retailers when you shop in-store (save your receipts and scan them in!), linking your loyalty card, and in-app purchases.

I don't like to coupon. Really, I kinda hate it. And I firmly believe you can't coupon your way to wealth. My thoughts on “couponing” changed when I met the Ibotta app.

- It helps me better optimize the rewards programs I do use (CVS) that I previously had a hard time keeping up with.

- $20 welcome bonus when you make your first 10 redemptions (took me one shopping trip at Publix.)

- Venmo or Paypal payment cashouts as soon as you get $20.

- Price: FREE. Download the free Ibotta app here.

Ebates ( now Rakuten)

How it saves money: Cashback rebates on your purchases with participating retailers.

Why I like it:

- On top of using the Rakuten app for cash back, installing the Chrome extension means you don’t even have to think about making sure to use the Ebates link first as you shop, it will just automatically prompt you when you visit the retailer.

- Honestly, I wasn't earning much through Rakuten until I downloaded the Chrome extension, so make sure to do that. You can download the extension for free here.

- It will prompt you – automatically – to activate cash back whenever you're at a participating retailing. I've earned over $400 in “Big Fat Checks”

- Price: FREE. Click here to download.

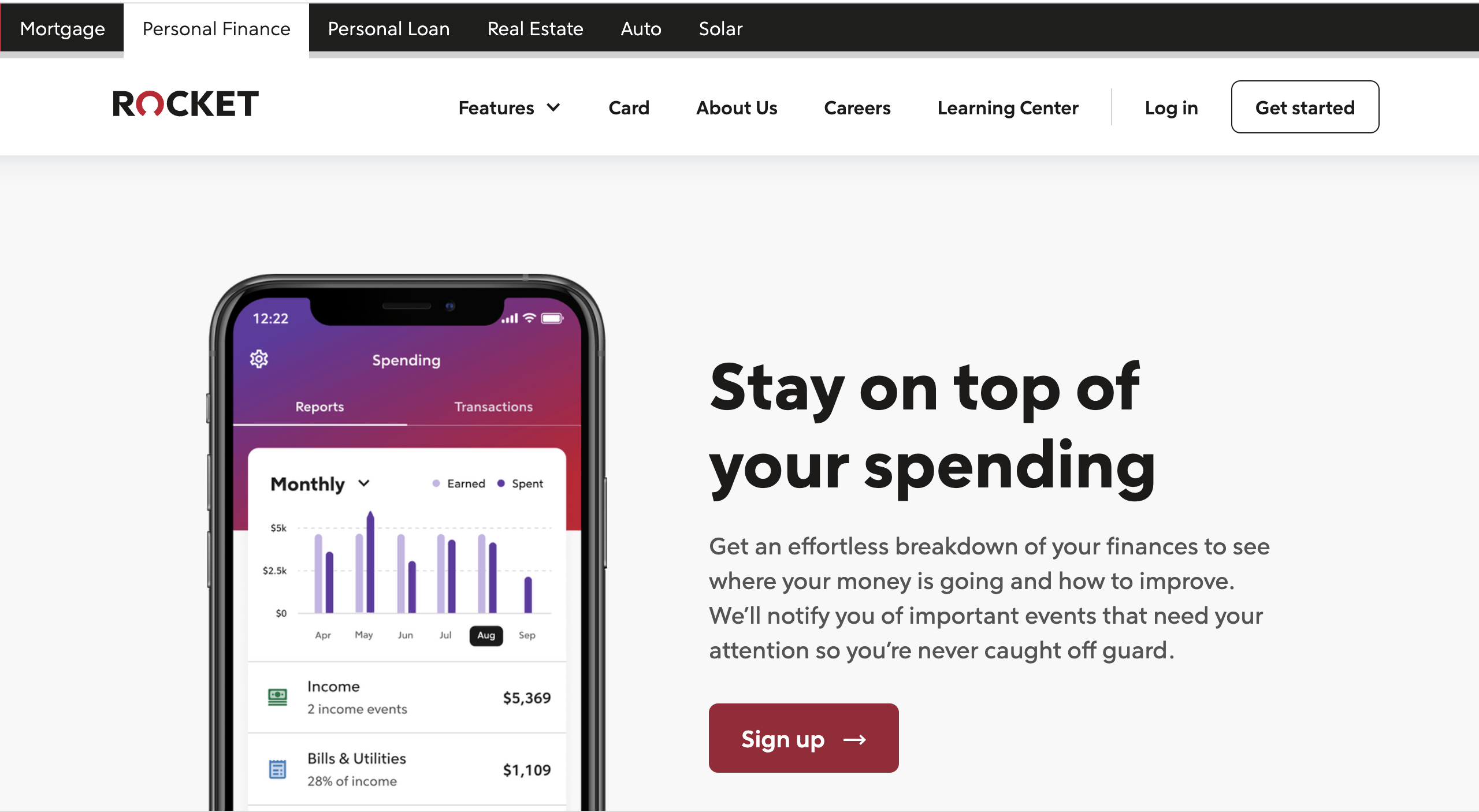

Rocket Money

- How it saves money: Keeping track of your money is always the best way to stay on top of a tight budget and make sure you're not overspending.

- Why I like it: A budgeting app that also works to cancel subscriptions on your behalf. Nice to have all of this technology/functionality in one place.

- Price: Free. Click here to download now.

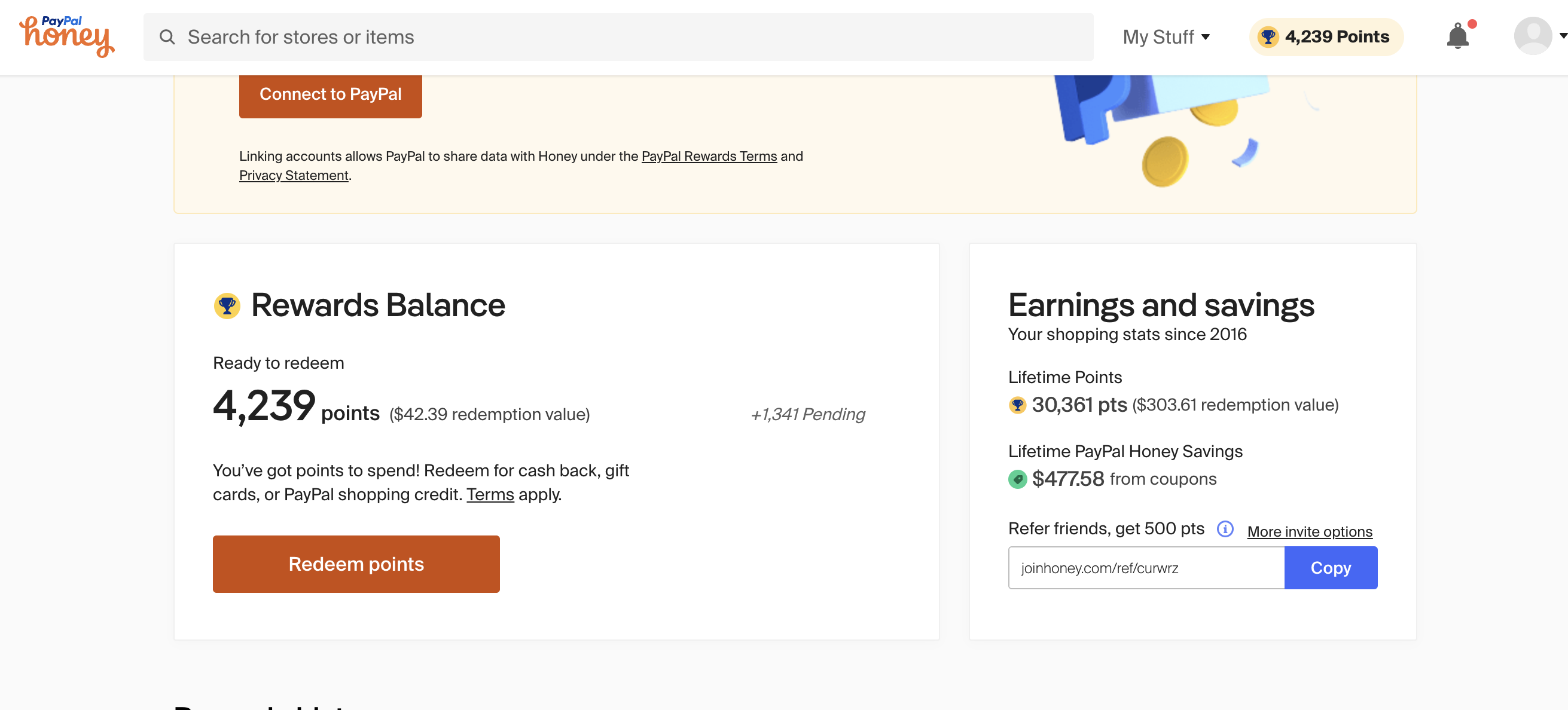

Honey

-

- How it saves money: Honey is the OG extension for scouring the web for a coupon code. I've both saved AND redeemed an eye-popping amount of money as Amazon gift cards through this one app/extension alone. (See screenshot above.)

- Why I like it: If you like to shop online (which, ahem…is me.) Then it's nice to have an extension finding the best codes for you automatically. If they don't have a working one (which is rare) I look myself, which is a 10-15 minute time investment, so it's nice a technology can do it for you…. saving both time and money. If I had to pick a #2 to Qapital, this one would be it!!

- Price: Free. Click here to try it.

Cleo

How it saves money: Cleo leverages AI technology to build a budget FOR YOU. And I'm a “keep a paper record” and “do it myself” elder millennial and I still thought this was cool. It also has additional features like spotting you money if you overdraft or helping you build your credit.

Why I like it: This is the sassiest little app. A real kick in the pants (which, honestly, sometimes I need.) Not only that, it uses AI to deep dive your banking data to show you trends over time, making it easy to notice your own shortcomings when it comes to spending and saving.

Price: Free.

The TL: DR

And personally, from experience, I know how annoying it can be to try app after app after app. If I had to recommend one of each, I'd say try Qapital for automatic saving and see how much extra you can save each month. Then, for money-saving, I suggest installing the Rakuten Chrome Extension which operates anytime you're buying something online. I buy 95% of stuff for myself and our household online, and I get about $2-300 dollars back with Ebates/Rakuten each year.

Pretty good, right?

Lauren Bowling is the creator of Financial Best Life. Writing about money since 2012 (formerly as L Bee and the Money Tree), Bowling is an award-winning blogger and money and real estate expert whose advice has been featured on CNBC, Forbes, CNNMoney, Elite Daily, Business Insider, Redbook, and Woman’s Day Magazine and more. After selling the site to a division of The Motley Fool in 2019, Bowling is now back as the owner and primary voice behind FBL and is excited to continue educating elder millennials everywhere about how to afford their best life.