How I made my first real estate investment with no money.

Many of you have been following my (long, horrifying, exhausting) home buying journey on this site over the last five years and we're about to come to the exciting conclusion! For those just tuning in on what happened with my first real estate investment, and how I started real estate investing with no money, here is the TL:DR.

- I bought my first home at age 26 using the help of a down payment assistance program.

- Thanks to an FHA Loan and generous down payment assistance, I paid only $1800 at closing.

- The project was stressful and I made a lot of costly mistakes thanks to working with a super sketchy contractor.

- The home was an extreme fixer-upper and I spent ~$60,000 renovating the home in the final quarter of 2013.

- I used a 203k renovation loan to fund the renovation project, so the costs were lumped into my monthly mortgage payment.

- I rented out rooms in the house and became an accidental landlord.

Taking on such a massive project as a first-time buyer and at a young age gave me a crash course in homeownership, and so I spent the last five years writing exhaustively about buying and selling. I even wrote a book about it because I felt there were a lot of things no one told me about home buying I really felt first-timers should know about.

Now, it feels like that chapter is closed. The final bullet point on the list above is that on September 28th, 2018 I closed on the home.

And the big payoff – I walked away with close to $150,000.00 on the sale. My first real estate investment with no money yielded a crazy 8,000% return. Here's how I did it.

Getting started with my first real estate investment (without any money)

(In my best Sophia from the Golden Girl's voice) “Picture it: Atlanta, 2013”

I'd been back in Atlanta for over a year. I was in love with someone I thought I was going to spend the rest of my life with, and that life included a home in Atlanta.

I felt the urge to buy, and after befriending Paula Pant from Afford Anything and falling in love with everything she preaches on her site, I was convinced it was a great move for me financially. (It was!)

Being an HGTV addict all my life, I thought it would be fun to get a fixer-upper. Honestly, I loved the idea of creating order from the chaos of a neglected home, to get to pick my own finishes and make chic design choices. Financially, I also knew I'd get a lot more “bang for my buck” if I picked a fixer-upper.

Working at a hedge fund for analysts whose job it was to research and pick “hot” stocks to grow the company's fund taught me a thing or two about how to conduct research for your own investments.

This was one part of the process I did correctly: I did very thorough research when it came to selecting a neighborhood: I read news clipping on developments within “in town” Atlanta, checked property records, and became very involved in following the progress of the Atlanta Beltline project.

I narrowed it down to three neighborhoods:

- Capitol View/Capitol View Manor (where I live now)

- Adair Park

- The West End

I ended up picking the home I'm in now because it had a ton of space (3 stories, 5 bedrooms, 2 baths) a great backyard that backed onto a city of Atlanta park and because I saw a lot of potential in the house.

It had high ceilings and lots of light and I had that “feeling” when I walked in where the hairs stood up on the back of my neck. You know the one when you just feel like something is “right?”

Making It Lucrative

My mortgage broker told me if I bought a foreclosure I could qualify for a downpayment assistance program through Invest Atlanta. So by buying a foreclosure in an “at-risk” neighborhood that had been hit hard by the recession, Invest Atlanta gave me a “soft loan” of $15,000 for me to use for closing costs, my downpayment, or to pay down the additional principal on the home. (Last time I heard, they're no longer offering quite so advantageous terms, but still offering down payment assistant in Atlanta!)

Invest Atlanta forgives $3,000 of the loan every year I live in the home as my primary residence.

This money was used for closing costs and the downpayment. $11,000 of that money went toward the downpayment/mortgage, the rest to closing costs, and I famously only paid $1800 out of pocket at closing for the Invest Atlanta program fee and closing attorney admin fees.

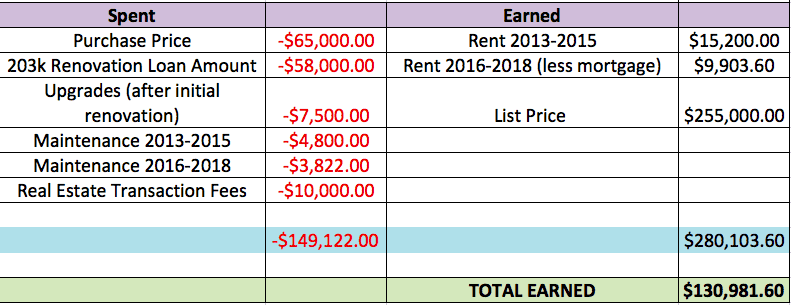

In this post (see: “How to Buy A Home in Your 20's“) I wrote that I bought my home for $65,000. I then had a contractor come out and bid the project and the home would need around $58,000 in renovations. As a foreclosure, the home had sat vacant for almost a year and all of the copper in the home was gone. Being that it was so old, it also needed a complete re-do of the plumbing, HVAC, and electrical systems to bring the home up to code.

So the numbers for my “no money” real estate investment are as follows:

- $65,000 home price + $58,000 renovations (which I lumped into my mortgage via a cool product called a 203k renovation loan)

= $123,000 - $123,000 -$11,000 (down payment assistance) =$112,000 mortgage (or about $915 each month after I pay the mortgage payment, private mortgage insurance, and escrow fees, which are all conveniently lumped into one payment.)

- Also, because I renovated a historic property (my home was built in 1941) I qualified for additional tax incentives. One is a “freeze” on my property tax for the next ten years, meaning even if my home value and the ones around me skyrocket, I'm locked in at the price I would have paid on a $65,000 dollar home (about $800 a year== SO CHEAP!)

- And then another credit I applied for and received was a state income tax rebate for three years. Between 2013 and 2016, I received $2400 back at tax time from this rebate.

The Total Numbers (All five years) Behind My “No Money Real Estate Investment”

These numbers don't include mortgage payments I made while living in the home as my primary residence.

Because the mortgage was around $100k at the time of sale, I received $147K+ and I'm really, really proud of my first home/real estate “investment.”

But the whole occasion (or lack thereof – I didn't even get to attend closing due to FinCon) got me thinking about what it takes to invest and make that kind of money with a real estate purchase, what I would've done differently, and where I'm at now.

Lessons I learned

“Good deals” are really rare

I'm putting a disclaimer here: My results are not typical and you should not expect to make that kind of money from investing or real estate investing. Housing has only gotten more expensive, particularly in urban areas and even more so in Atlanta. Maybe in a smaller town a fixer-upper can be had for under $100k, but I haven't seen prices like that in a while.

Even though studies show how millennials are economically disadvantaged because of the recession, I was able to economically benefit from the housing bust. Not only was I able to get a home at a rock-bottom price, but my interest rate for the home was a super-low 3.25%.

My fiance´ and I are now under contract on our first home together currently and, trust me, the interest rate is not 3.25%.

Five years is a long time

Initially, when I applied for downpayment assistance and learned it would be forgiven over five years I thought, “Oh, five years isn't so long. I can do that.”

But standing at the end of it looking back, a lot has transpired and changed since 2013. Five years was much, much longer than I ever anticipated.

But it taught me an important lesson – that with any investment you have to be patient. (And anyone will tell you patience is not a virtue of mine.)

When it comes to earning money, nothing happens overnight. Nothing. Not a business, not an investment, not debt payoff. There is no such thing as a “get rich quick” scheme.

When it comes to wealth building, you have to redefine your definition of “quick.”

Frame Your Thinking Around How to Make Your Money Earn Money

I'm not sure if I've ever shared why I went down this road in the first place. I think I've probably talked about it on a podcast or in an interview at some point or another, but basically when I left my full-time job in NYC they gave me the rest of my bonus as severance and for the first time in my adult life I had legit savings. After taxes it ended up being around $16k at the time.

(Also – figuring out how to live frugally to make that money stretch became the impetus for this blog…. but that's another story for another day.)

After five months of unemployment and getting established in my own apartment in Atlanta, I only had about $8k left the following year and knew if I didn't put it someplace where it could make money and grow, then I'd be likely to squander it all.

Because I'm a big spender and recovering shopaholic.

But mostly, I wanted the money to mean something; I'd had a hard time in New York (which I won't go into too much detail here – it's in the past) but basically, I wanted something tangible and real.

Something important where I could look back and say, “I have (x) because of (y).” I felt it would help me make peace with the situation and also help provide some stability and real roots in my life during a very chaotic and confusing time in my life.

So, I decided to put the remaining money into a small, low-cost piece of real estate. It wasn't until I did more research that I found I could get the assistance if I renovated and then from there, I found a house I felt had potential and from there it's history.

It's always more work (and expense) than you'll plan for

The abbreviated version of my story above probably makes it look really easy. And many will say I got “lucky,” but there really isn’t any luck involved when you buy a home in an underdeveloped area. My choice in housing was very much intentional.

Here's all the work I did over the last five years:

- Doing the homework for the purchase – the due diligence on the neighborhood, research on my down payment assistance.

- Tirelessly searching for properties near the Atlanta Beltline development project, which I knew and began to see were majorly impacting real estate values in areas where the Beltline had already gone in.

- I did the things most people wouldn't do – like and buy a home in an less desirable area. In order to generate any kind of wealth, you have to be willing to do the things most “normal” people wouldn’t do.

- For a few years until my finances recovered, I had to live on a pretty bares bones budget.

- I stayed in on Friday nights to work on the blog or do freelance writing projects to make more money.

- I was only making $40,000 at the time I bought the home, and so had to “house hack” by renting out rooms and live there at the same time. It was work to get the home ready to rent, manage personalities of different roommates (it took a few tries to find a good one), and keep the house in order.

- In terms of expenses, I didn't travel a ton (not like I do now) those first few years because most of the spare monies I had went back into repairing and maintaining the home.

When people say it was “luck” ….It's irritating because there was so much work involved. But all you'll see is my clickbait title and smiling face in the cover photo, won't you?

You have to be willing to do what no one else will

I have a favorite mantra of late and it's one I repeat over and over (especially when I don't want to go to the gym.)

“To live the life you've never lived, you have to do the things you've never done.”

And this is where so many people trip up. Success isn't accidental and you have to be willing to put in the work.

And I also think success requires a certain amount of risk tolerance. At the end of the day, my “real estate investment,” was a risk. While I felt very good about the investment, there wasn't a guarantee it would work out. The neighborhood may not have appreciated in value, or at least at the rate it did. I had to be okay with both the success and the failure.

There's really no nice way to put it. In 2013 I moved into a really run-down neighborhood.

It'd been hit hard by foreclosure and many of the homes weren't well cared for, or boarded up and sitting vacant and abandoned. However, the neighborhood felt very”up and coming”, with a few renovated homes and an active and friendly homeowners association, so I went for it and had a (mostly) great time.

At the time, almost everyone (parents and best friends) thought I was making the biggest mistake of my life.

Not to mention putting my own safety at risk.

After my then-fiance and I broke up, my parents begged my younger brother to move in with me so I wouldn't be alone there at night. He graciously agreed and I ended up dedicating my book, The Millennial Homeowner, to him.

But no matter how chaotic and stressful it got, I always knew I was doing it to have my money make money.

I always knew after five years of people making fun of me for living in that neighborhood, friends too scared to visit and leave their car outside, and people wondering if I’d actually lost my mind, that I’d be the one laughing.

I always knew that the initial $1800 would grow into something much bigger.

Frequently Asked Questions about Real Estate Investing with No Money

What should I know if I want to use down payment assistance?

You read in the first paragraph. I bought my first home for $1800. It definitely took some research and money savvy, but you too can buy a home for cheap…and it doesn't require a finance background or degree, which is why I wanted to share my story.

One BIG thing I did do right in my first home purchase was that I researched the crap out of every down payment assistance and grant program that I could find.

In 2013, the city of Atlanta was offering $15,000 in down payment assistance grants to first-time homeowners who purchased foreclosures in certain neighborhoods.

It was a good bit of paperwork, but in return, I received $15,000 in down payment assistance.

It's not free money. Rather it was a “soft loan” that got forgiven a little bit each year. I also could use the money however I chose–for the down payment, principal or both.

But I only had to pay $1,800.00 at closing, which is almost unheard of. Not to mention that ~$1800 is what many people pay for first month's rent and deposit on an apartment that they don't even own.

Still, taking on a downpayment assistance program with a lot of stipulations may not be for everyone.

This is why it's important to assess your priorities and values before buying a home, which is something I discuss at length in my book, The Millennial Homeowner. Maybe you want to live in a better area, don't want a fixer, or maybe you just want your first home purchase to be (fairly) seamless the first time around. That's perfectly okay! Still, for those of you who have a limited budget or simply want to make a strong real estate investment, I outline my tips and tricks below.

Tip #1 -Ask Around

Your mortgage broker or real estate agent may mention down payment assistance programs to you, or they may not, which is why it always makes sense to ask. If you're in the beginning stages of the home buying process, do a little internet research of your own.

Just get started by opening up your browser, getting a new window, navigating to google and type in {[state you live in] downpayment assistance programs}. Boom. Or you can check your eligibility on Downpaymentresource.com here.

Veteran? Single Mother? You may qualify for additional grants and funds. Now isn't the time to be shy, but you have to ask around for those too.

Tip #2– Get Organized

Any program you may qualify for is going to take a lot of paperwork and patience during the application process. After all, nothing comes free. If you want that money, you're going to have to invest the time into getting it. I recommend in this post to get organized with all your documents before you start actively searching for a home, and if you've done this well, the whole shebang will go a lot smoother.

You're going to have to pull tax records, employment forms, W-2's, W-9's and (potentially) other weirder demands like letters from former landlords, lovers, and family members.

Often it's the time and paperwork that keeps many (lazy) people from applying for these funds. In my opinion, that is leaving money on the table.

For about six hours worth of effort pulling documents and filling out paperwork, I received $15,000 in downpayment assistance from the city of Atlanta.

This was very worth it to me as with this money I was able to cover all but $1800 of my down payment, my closing costs, and put a little extra toward the principal on my first home.

Tip #3 – Assess if it is right for you

Some programs (like mine) require you buy a home in a certain zip code in order to qualify for the moolah. Like in the case of the assistance I received, I was only eligible if I bought in a neighborhood hit hard by foreclosure. This is a dainty way of saying, “up and coming,” which is a daintier way of saying, “run down.”

I had doubts at first. Friends and family are terrified to come over. But honestly, I've never had a problem and the neighborhood has turned around a lot, as I expected it to when I was doing my due diligence. My program allowed me $15,000 dollars. That's a lot of money.

Honestly, if someone came up and offered you a check for 15k to live in an up-and-coming neighborhood, what would you say?

Maybe because I'm a more finance-minded person, I took the chance. And because the house was setting off my spidey sense that it would offer the greatest opportunity for a strong return on investment.

Still, it was a slow play. My investment was definitely a long game and down payment assistance programs aren't for big-time investors.

But it's up to you to decide what you need in your home and its location.

Tip # 4 – Actually Read the Fine Print

Some programs only allow for the money to go toward the downpayment and no closing costs, some vice versa, and some allow for both. Be sure to read the fine print of your program's terms to understand how much assistance you're getting as well as the expectations and repayment requirements (if any.)

Ideally, you'd want your program to allow for funds to be used at closing, as this is where first-time buyers incur the most out of pocket expense, in addition to the inspection and any unexpected repairs.

That 15,000 helped pay for my down payment, most of the closing costs, and a little bit of the principal on the loan. The $1800 was my own contribution and a $1000 program fee. I would have had to bring double that amount had I not used the down payment assistance.

What I’m going to do with the money from the sale of my first real estate investment

I announced this on the ‘gram, but Rich and I are in the process of buying our first home together. While I can’t share any details yet (we close on October 31st!) I can say that we are in a dream neighborhood, it's move-in ready, and we’re both super excited.

It makes me smile to think that five years ago I was living in one of the most downtrodden zip codes in Atlanta, and now I’ll be able to afford to live in one of the best.

So, a large chunk of the money will be for my half of the down payment. But, the rest will be split:

- Making close to $30k in retirement “catch up” contributions

- Buying a new car (when the time comes.)

- Having a nice nest egg in both my personal and business savings accounts (so I no longer have to sweat whenever I want to invest in the business or pay my taxes or when clients pay me late. )

- Starting a real f*ck off fund.

I'm also contemplating what my next investment will be. As I said above, I need to think about how I can make this money earn more for me, but TBD on what that will look like.

And while $150,000 isn’t enough to retire on by any stretch of the imagination, my little nest egg should keep me from having to seriously worry about money ever again, so long as I continue to earn, spend, and save wisely.

Lauren Bowling is the creator of Financial Best Life. Writing about money since 2012 (formerly as L Bee and the Money Tree), Bowling is an award-winning blogger and money and real estate expert whose advice has been featured on CNBC, Forbes, CNNMoney, Elite Daily, Business Insider, Redbook, and Woman’s Day Magazine and more. After selling the site to a division of The Motley Fool in 2019, Bowling is now back as the owner and primary voice behind FBL and is excited to continue educating elder millennials everywhere about how to afford their best life.